Introduction

A lot of pandemic era stocks lacked basic unit economics, and were found out when the funding stopped and subsequently collapsed. Some had network effects / unit economics, but needed to ‘get fit’ (think Uber and Meta), some have righted their mid-pandemic wrongs with clear turnaround / value creation plans and been rewarded (think Carvana), and some have righted the wrongs but not yet been rewarded. I think Fiverr sits in this latter category.

Fiverr is a leading freelance marketplace which connects businesses with freelancers offering a wide range of services.

The following analysis breaks down Fiverr’s business model, operating model, financial performance, competitive landscape, and more from the lens of a prospective investor. I also briefly at the end compare Fiverr to its main competitor, Upwork. Overall Fiverr and Upwork are highly volatile stocks (90%+ drawdowns from the peak), so not the type to be invested in by the feint hearted.

About the company

Founded in 2010 by Micha Kaufman and Shai Winiger in Tel Aviv, Fiverr operates a two-sided marketplace matching small businesses with freelancers. With approximately 700 employees, Fiverr is listed on the New York Stock Exchange ($FVRR) and had a market cap of just under $1 billion in June 2024, down from about $11 billion during the COVID-19 pandemic.

Problem statement Fiverr solves

Fiverr transforms the opaque and inefficient process of hiring freelancers into a modern, user-friendly e-commerce experience.

Unique Selling Proposition (USP):

Fiverr offers an easy-to-use platform where people can buy and sell small services for a flat starting fee. The platform boasts a comprehensive catalogue of services and well-vetted freelancers.

Potential sources of network effects:

- Buyers: Around 4 million buyers, with approximately 65% of core marketplace revenue from repeat buyers, indicating sustained user engagement.

- Service Categories: Over 700 freelance service categories, including recent additions like AI content and development. Gigs range from $5 to $50,000.

- Freelancers: Approximately 400,000 active freelance sellers.

Investment Thesis

Star Company

Fiverr operates in a profitable and growing market niche (SMB freelance digital services) with growth exceeding 10% per year. It is a leader in its niche, matching freelancers to smaller SMEs effectively. This makes it a ‘Star Company’. I only invest in Star Companies and have explained why in this article.

Reasons why I think the stock will rise

- Overly Beaten-Down Tech Stock: Fiverr, has seen its share price decline by over 90% from its February 2021 peak. This significant drop – which has also recently been exacerbated by the geopolitical concerns in Israel and Palestine and the disruptive impact of AI on its business – is a common trend among tech stocks that were COVID-19 beneficiaries. What seems to have been overlooked is Fiverr retains a very viable and growing business post pandemic.

- Shift to Profitability and Cash Generation: Fiverr’s growth has slowed to approximately 10% year-over-year as it has pivoted its focus towards profitability and cash generation, addressing investor demand for a focus on fundamentals. This strategic shift is reflected in improved bottom-line results, including free cash flow (FCF) and earnings per share (EPS), underpinned by key performance indicators like higher average ticket sizes and growing gross margins.

- Attractive Valuation Metrics: Following recent share price pressures, Fiverr currently trades at a 2024 forecast earnings/enterprise value multiple that is attractive (c. 8.6x) given its 10% growth rate and acceleration in key value creation metrics, including EPS, FCF per share, and return on invested capital (ROIC).

- AI concerns appear overblown: Investors are concerned AI will disrupt the services provided by freelancers on Fiverr’s platform, but Fiverr’s Q1 2024 results exceeded expectations, leading to raised guidance for the full year. Management has highlighted the net positive impact of AI on the business.

- Stable Take Rate and Financial Resilience: Fiverr’s take rate remains stable at 30%, it has a $304m net cash position, and the company is free cash flow positive, providing significant financial resilience. I.e. it has gotten beyond ‘default alive’.

- Dynamic Macro Environment: While the macroeconomic environment remains challenging with constrained budgets in large enterprises and financial pressures on small businesses, Fiverr’s high exposure to smaller businesses positions revenues to rebound quickly as conditions improve.

- Share Buyback Program: In May 2024, Fiverr initiated a $100 million share buyback program, reflecting management’s belief that the stock is undervalued. They are confident in their cash position and free cash flow generation to support this initiative.

- Large Short Float: The short float was around 10% as of June 2024, indicating the possibility of large upwards price moves if sentiment on the stock changes, as I think it should.

Overall, Fiverr’s strategic focus on profitability, robust financial health, and proactive management of market challenges make it a compelling investment opportunity.

Things I Don’t Like About the Stock

- Share-Based Compensation (SBC): The level of share-based compensation appears excessive and results in significant dilution. Deducting SBC from free cash flow results in a near zero number, meaning free cash flow per share is not trending up as quickly as desired.

- AI Cannibalization threat: AI has the potential to cannibalize certain services offered on Fiverr, such as logo design and article writing, which could impact revenue.

- Buyer Trends: While the number of buyers has been declining, this has been offset by an increase in the average purchase price. This trend is concerning and needs to be monitored.

Current position

I hold a small long position entered at an initial entry price of approximately $27 in Q4 2023. As of June 2024, the price is $24.5, down 10% from my initial position.

I researched and wrote down by thoughts in this article as way to determine whether to sell or increase my position.

My view is the stock has good chances of getting to c. $45 in the next two years, while the downside risk feels relatively low in the context of improving metrics and low valuation multiples. As such i intend to increase my position.

Things that might make me change my mind

- Revenue Contraction: A significant decline in revenue would be a red flag and could prompt a sell decision.

- Declining Take Rates: If Fiverr’s take rate starts to decline, it would indicate weakening network effects and competitive pressure.

- Declining Free Cash Flow Per Share: A consistent decline in free cash flow per share, would suggest operational issues or increased dilution from share-based compensation.

- Evidence of negative AI Impact: Any clear indications that AI is having a net negative impact on Fiverr’s business.

- Insider Selling: Significant share sales by senior management, which could provide advance warning for a lack of confidence in the company’s future prospects.

- Better alternatives: Identification of investments with a better risk/reward profile

Share Price Performance

Candle Chart Analysis

The monthly candle chart for Fiverr shows the following trends:

- Trend Identification: Significant upward movement from April 2020, peaking in February 2021, followed by a sharp downward trend. Since mid 2023, the stock has been ‘basing’ / chopping around in what looks like a ‘Stage 1’ position

- Volatility: The length of the candles and wicks indicates how much the stock’s price fluctuated during each month. Recently, the volatility has been relatively low.

- Support and Resistance Levels: Support around $20 and resistance at approximately $30.

I have set out below the current Analyst price targets. I.e. the current price of around $24.5 is the low. The high is around $45 in June 2025.

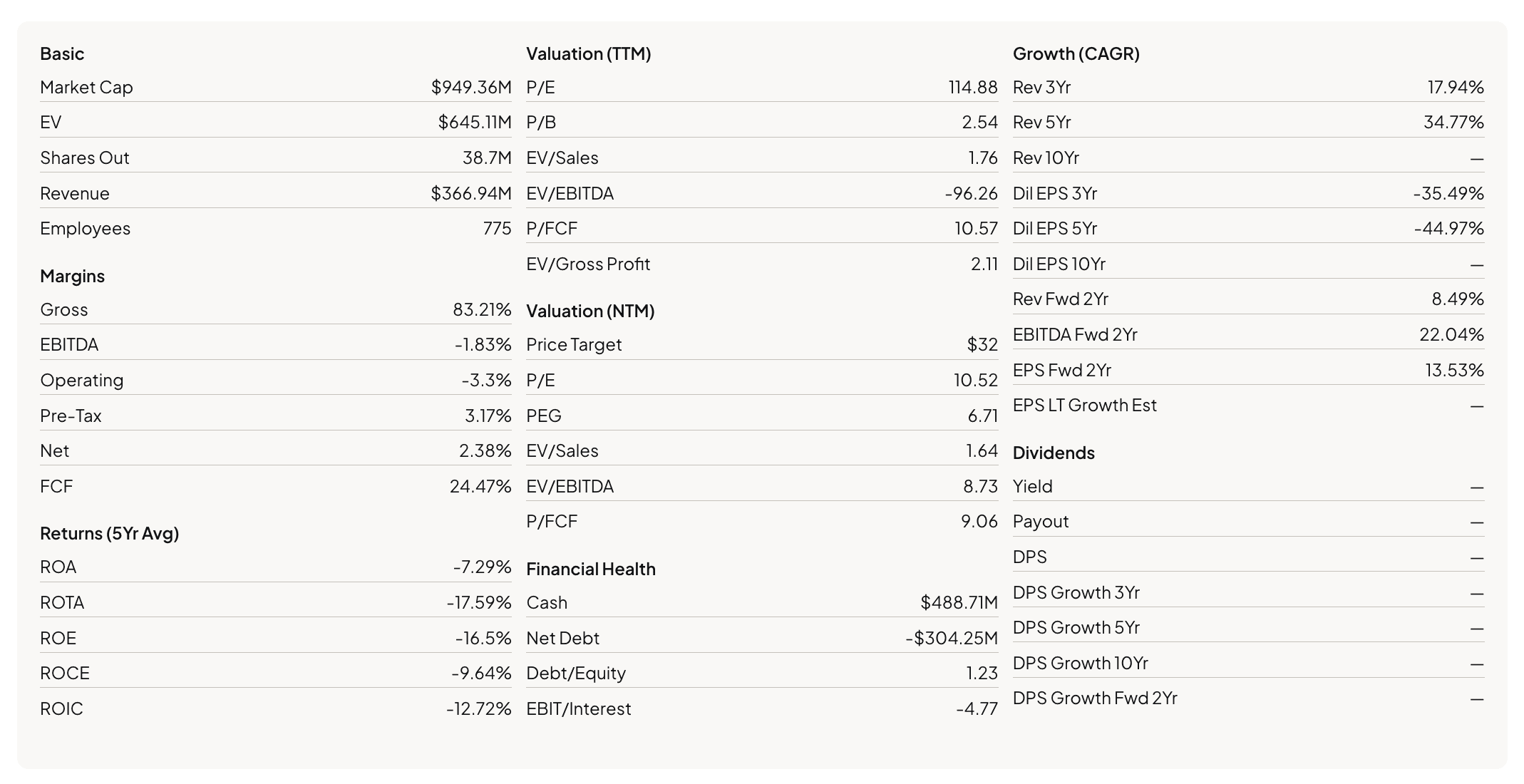

Summary of key metrics

A table setting out Fiverr’s key metrics is provided below:

- Revenue: $387 million forecast for FY24, representing a 7% year-on-year growth. Fiverr has a history of beating its targets.

- Gross Margin: Currently around 83% and growing.

- Net Cash Position: Approximately $488 million.

- Free Cash Flow: Positive, driven by high renumeration via SBC (non-cash).

- Share-Based Compensation: High at around 20% of revenue, causing shareholder dilution.

- Take Rate: Steady at around 30%.

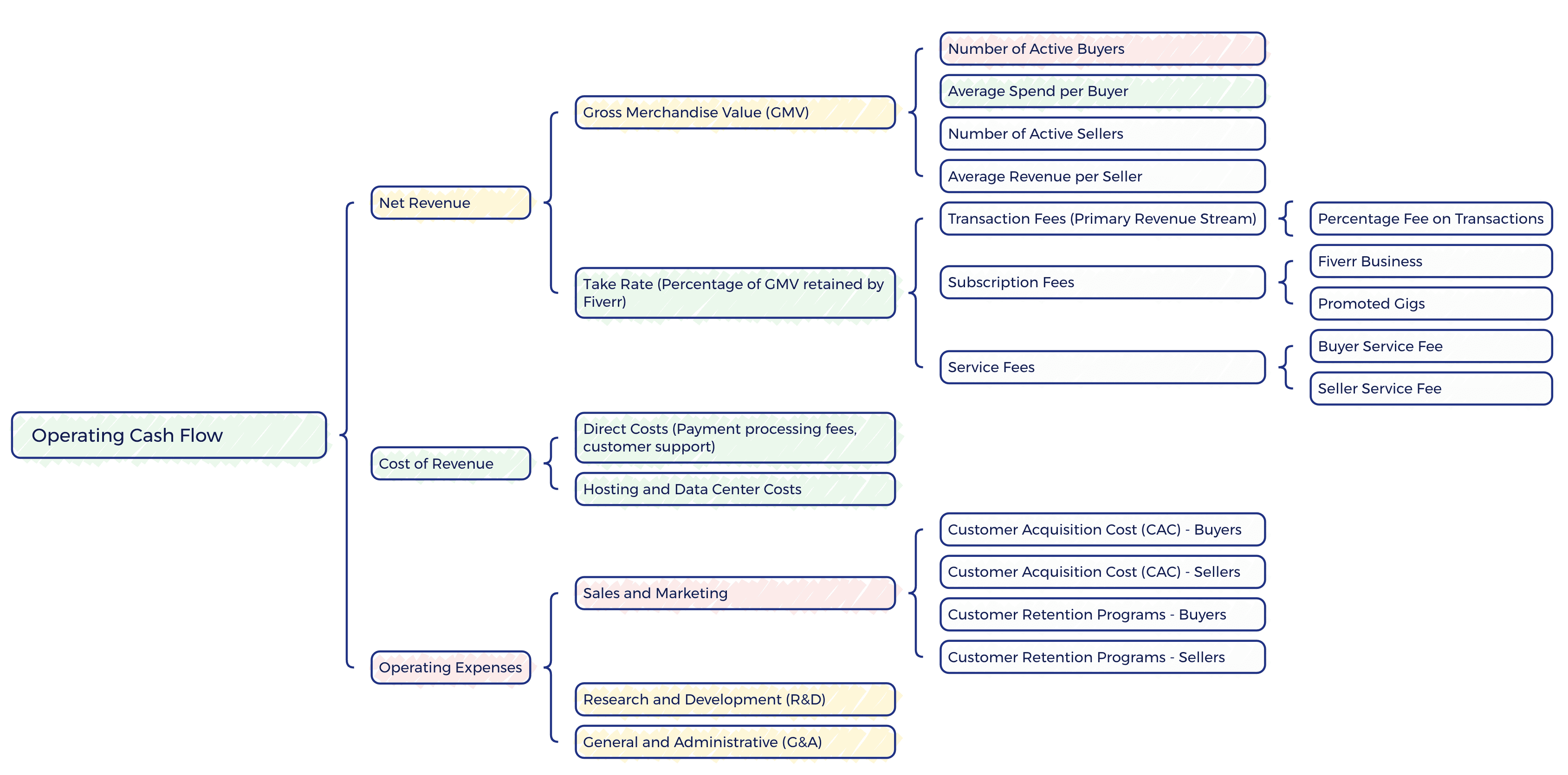

Value Drivers

I have set out the value driver tree for Fiverr below, with a RAG rating for the ones which are somewhat publicly available, which i discuss in more detailed below.

Fiverr’s value creation drivers / metrics include:

- Number of Active Buyers: Maintaining and increasing the number of active buyers is crucial for GMV growth. Active buyers drive demand for freelance services on the platform.

- Number of Active Sellers: A large pool of active sellers ensures a diverse range of services and competitive pricing, attracting more buyers.

- Spend per Buyer: Increasing the average spend per buyer through upselling, cross-selling, and expanding service offerings boosts GMV.

- Spend per Seller: Encouraging sellers to offer higher-value services and packages can increase the overall spend per seller, contributing to GMV growth.

- Retention Rates: High retention rates for both buyers and sellers are essential. Repeat business from satisfied customers and sellers drives sustainable GMV growth.

- Geographic Expansion: Expanding into new regions can bring in additional buyers and sellers, contributing to overall GMV growth.

- Service Category Expansion: Introducing new service categories, especially high-demand areas like AI services, can attract more buyers and increase GMV.

- Platform Enhancements: Continuous improvement of the platform’s user experience, including better matching algorithms and new features, can drive higher engagement and spending.

- Operational Efficiency: Focus on improving gross and net margins through cost management and scaling operations.

- Technology and Innovation: Leveraging AI to enhance service matching and platform efficiency.

- Market Position: Leading the SMB freelance digital services market with a strong brand and loyal customer base.

- Financial Resilience: Maintaining a strong balance sheet and positive free cash flow.

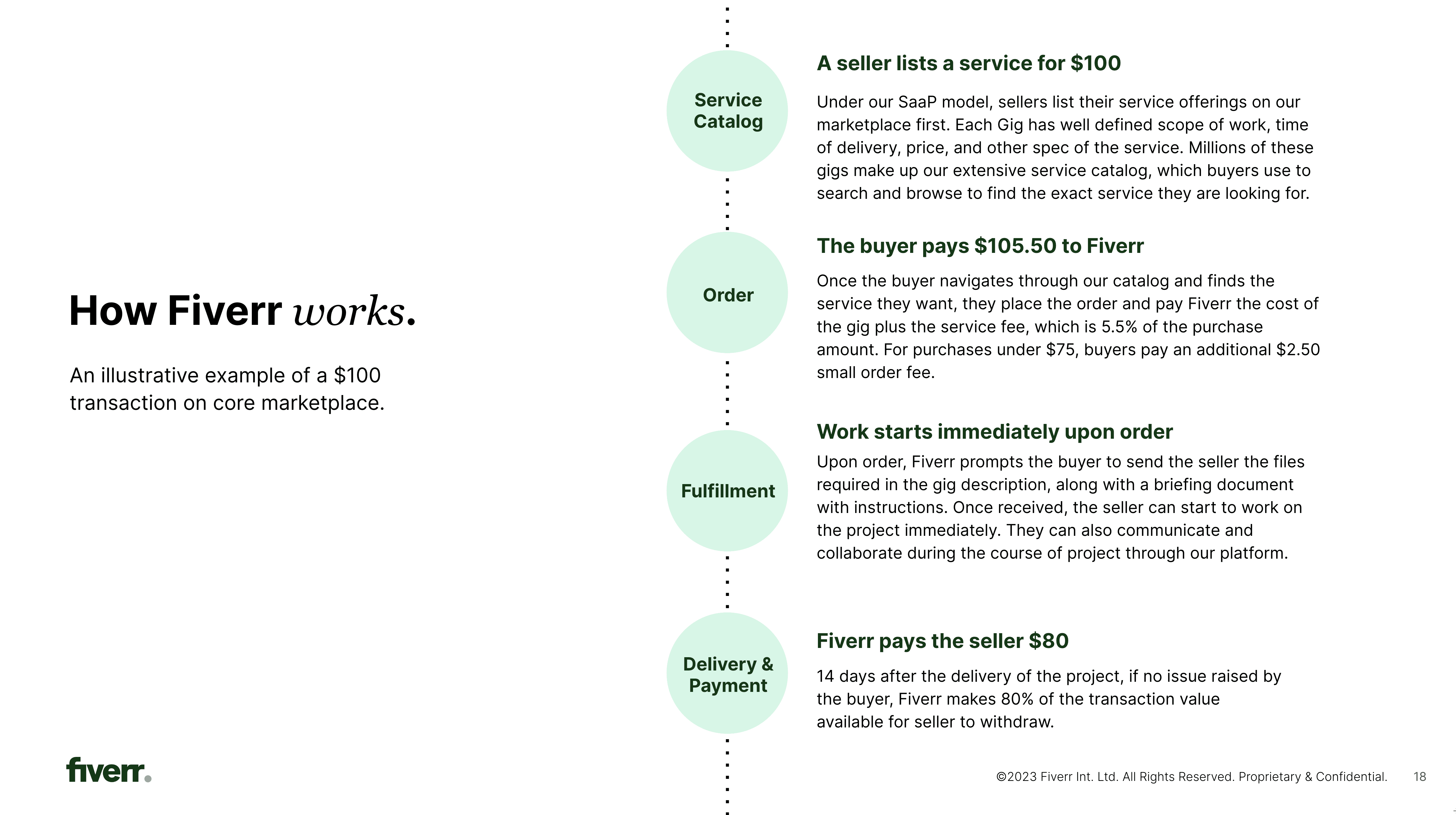

Monetisation

Fiverr monetises it’s buyers and sellers as follows:

- Buyers pay 5.5% (plus $2.50 for small orders, I think $75)

- Sellers pay 20% commission.

- Fiverr’s take rate is a combination of those, plus optional subscription and service fees like ‘Seller Plus’ and ‘Promoted Gigs’.

Overall the take rate adds up to an average of c 30%, and has been stable at this level for a long period.

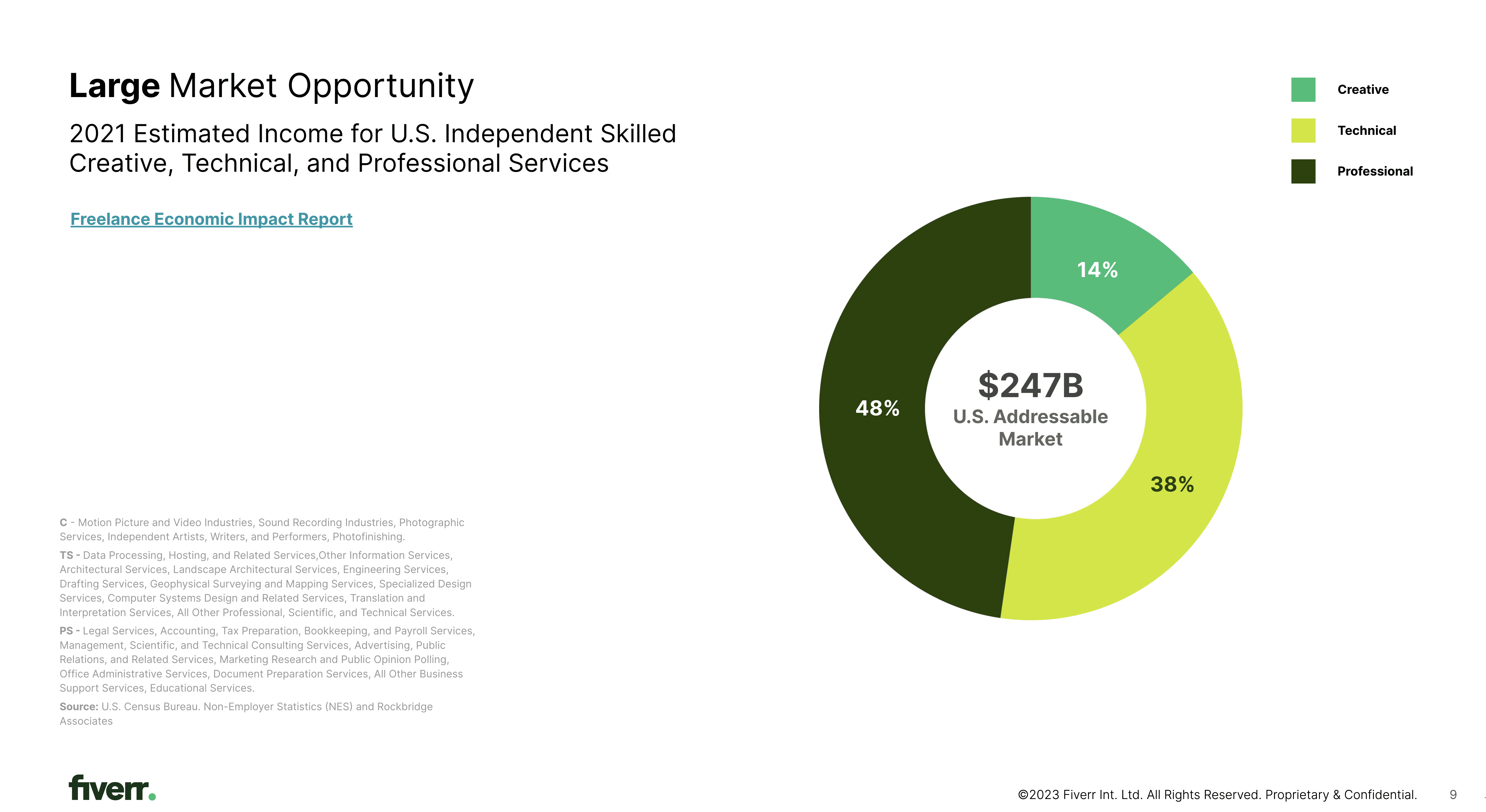

Addressable market sizing and key growth opportunities

The below is Fiverr’s estimate of the addressable market market in the US – i.e. USD 247bn. Most of this is currently offline. In FY23 Fiverr’s global GMV was only c. USD 1.2bn – so less than 0.5% of the global addressable market.

Key growth avenues include:

- Deepening penetration in the US

- Increasing retention and purchase frequency / value

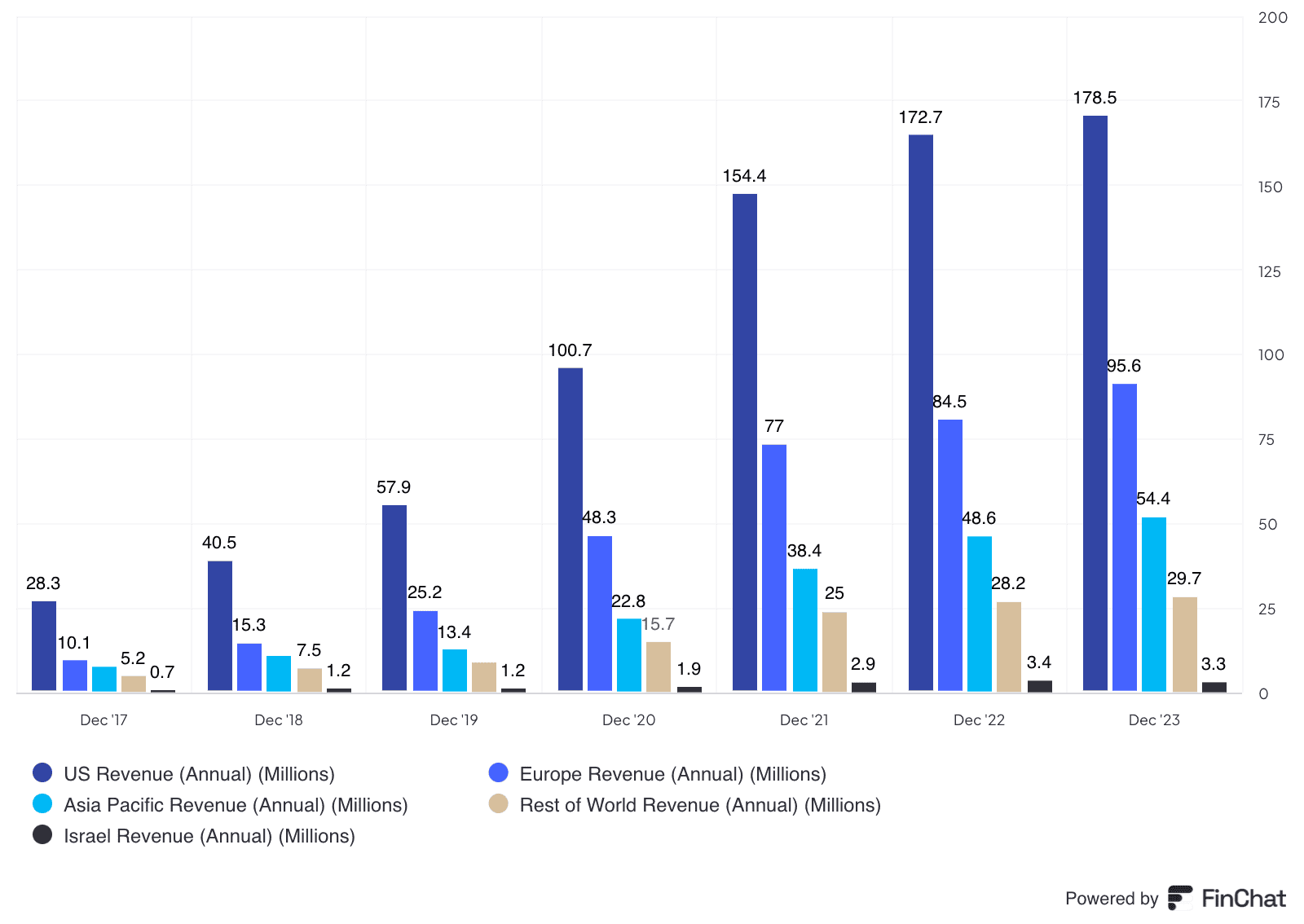

- Geographical expansion of buyer base outside of core US market – recent success in the UK, Germany and France

- Horizontal service expansion, including AI implementation services

- Moving up-market for buyers and sellers

Buyer KPIs

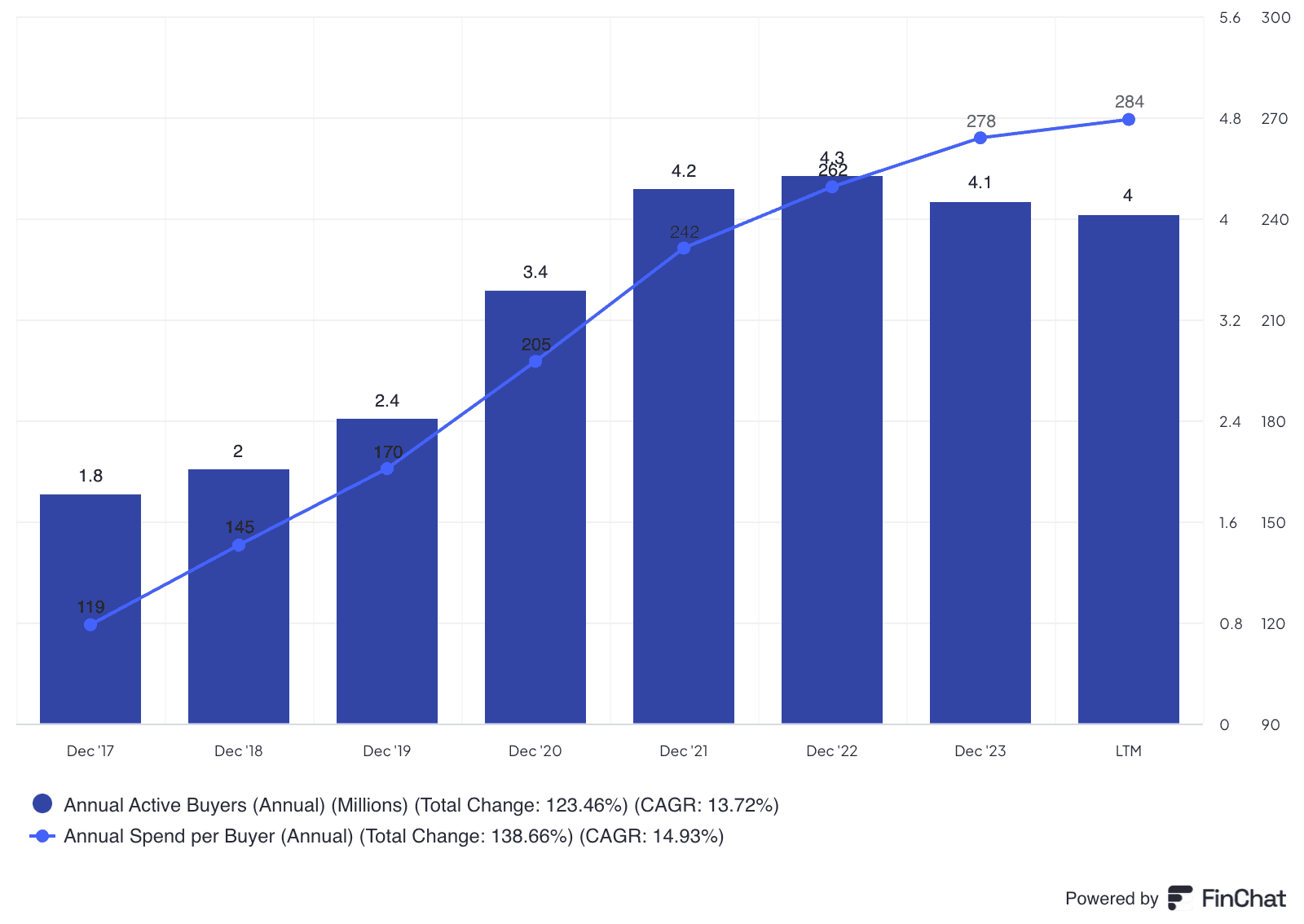

The key buyer trends are:

- Number of active buyers is flat / falling

- Spend per buyer going up – loyal customers enjoy the service and there is a greater focus on high-value buyers.

In addition, the take rate has been flat at 30% for a number of years – indicating fiverr has network effects due to the ability to command high takes while retaining buyers.

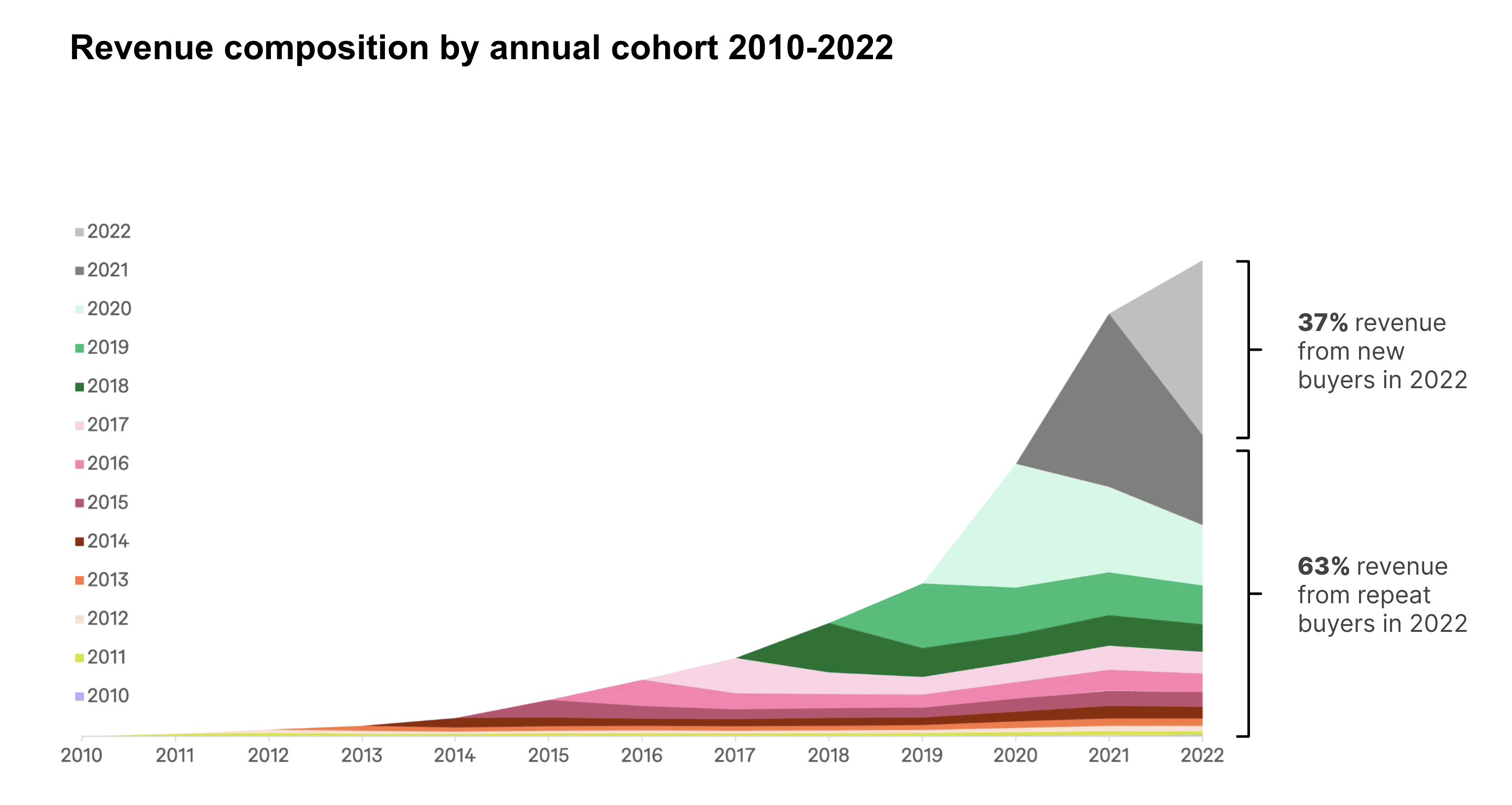

Cohort data shows consistent behaviour across cohorts, with the majority of revenue each year from repeat buyers.

Key financials

Revenue & Earnings Trends

Annual trends

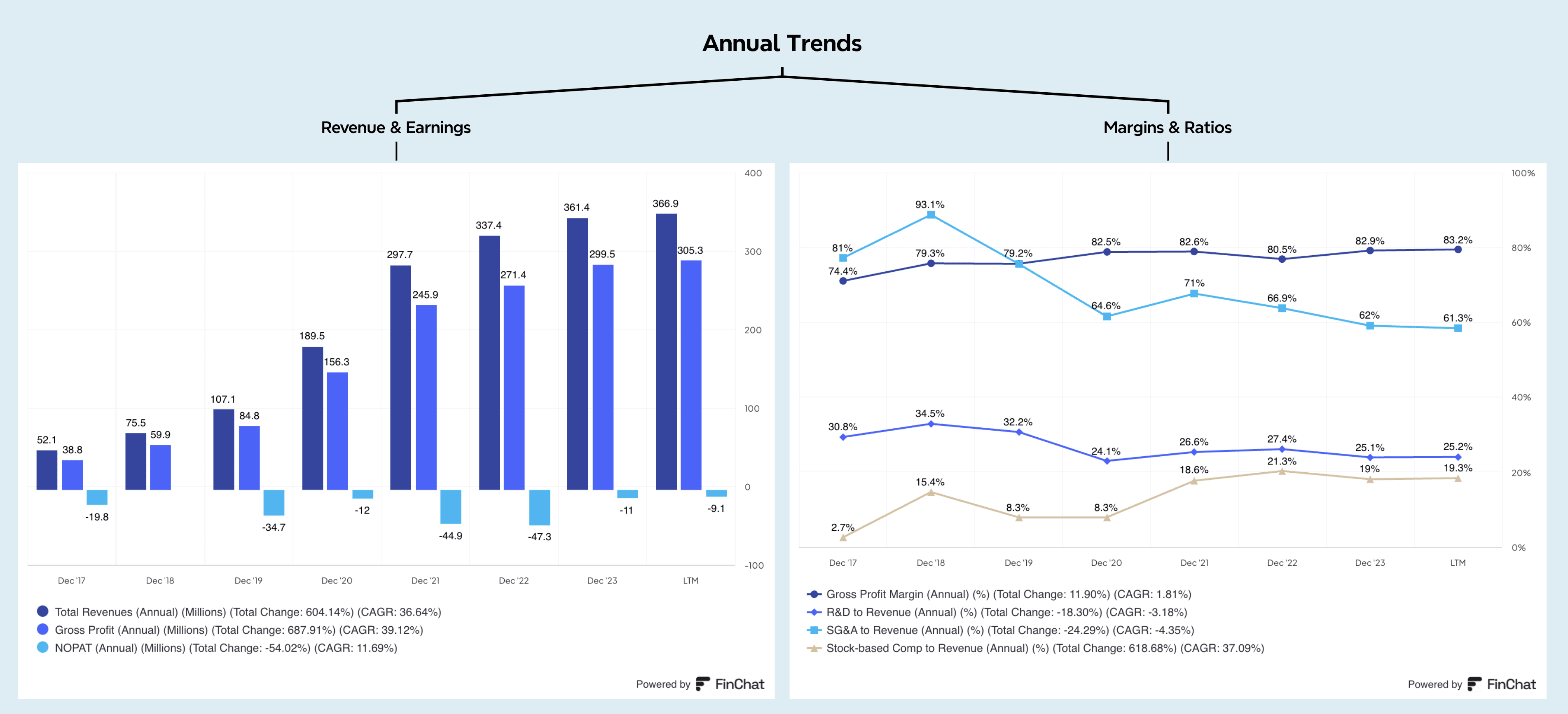

Revenue Growth: Fiverr’s revenue and gross profit have scaled significantly, currently about 3.5 times higher than at IPO in 2019. However, growth has slowed since 2022 as the business focuses on profitability.

Gross Margin: High at approximately 83%, indicating efficient operations.

SG&A Costs: Reduction in SG&A to revenue ratio from 80-90% in 2017-2018 to around 65% in 2020. However, share-based compensation as a percentage of revenue has increased from 8% to about 20%, which is concerning.

Fiverr has project FY24 revenue of USD 387 million, i.e. a 7% year on year growth, driven mostly by improving take rate (with 1% GMV).

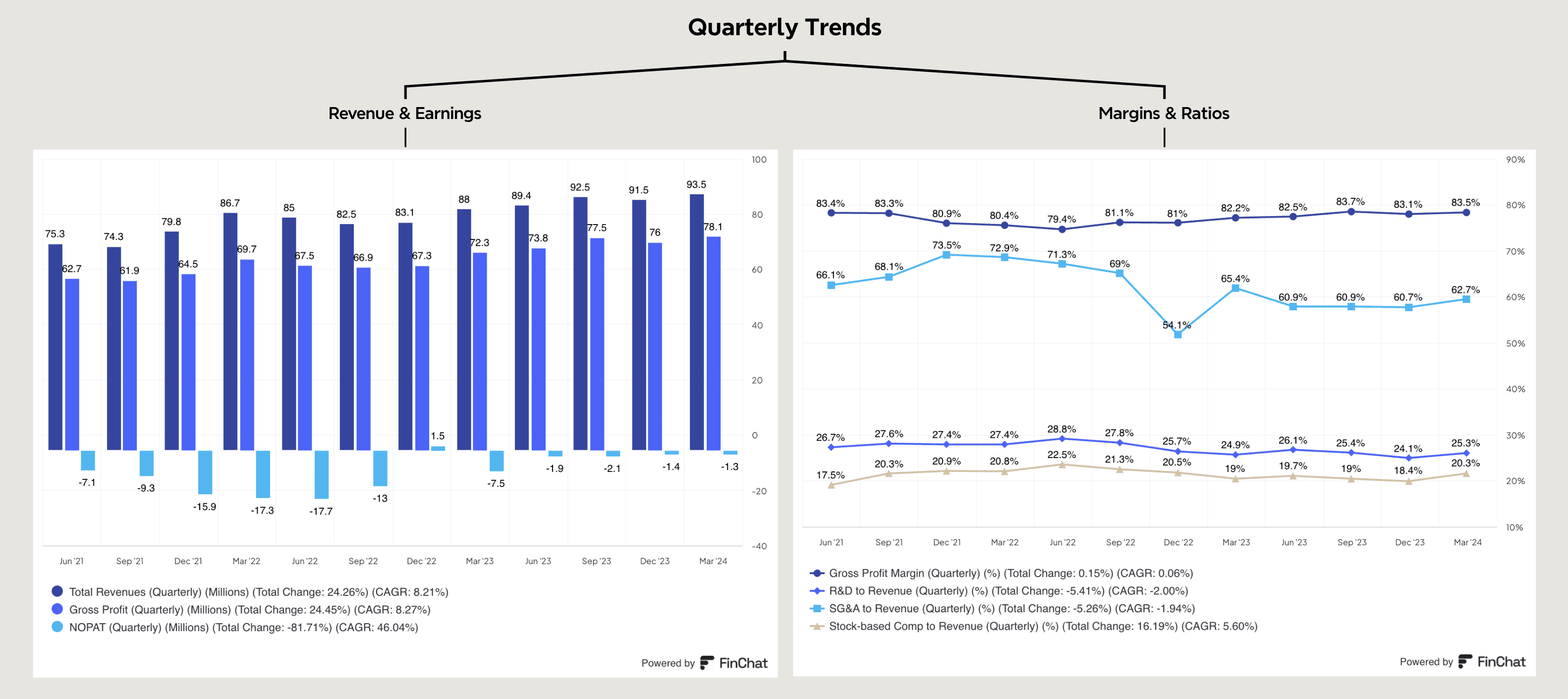

Quarterly trends

Steady Progression: Positive quarterly progression in revenue and gross profit.

Approaching Breakeven: Net operating profit after tax is nearing breakeven, with net income positive since Q3 2023 due to interest on cash.

Share-Based Compensation: An uptick in SBC to revenue in March 2024 is a negative trend.

To be driving economic profits of c. 20% plus, the SG&A cost needs to come down significantly to around 40% of revenues inclusive of SBC. This ultimately requires higher revenues (potentially driven by more add income) or better operating leverage through lower SBC % of revenue, less marketing spend due to a greater proportion of organic growth or better R&D efficiency.

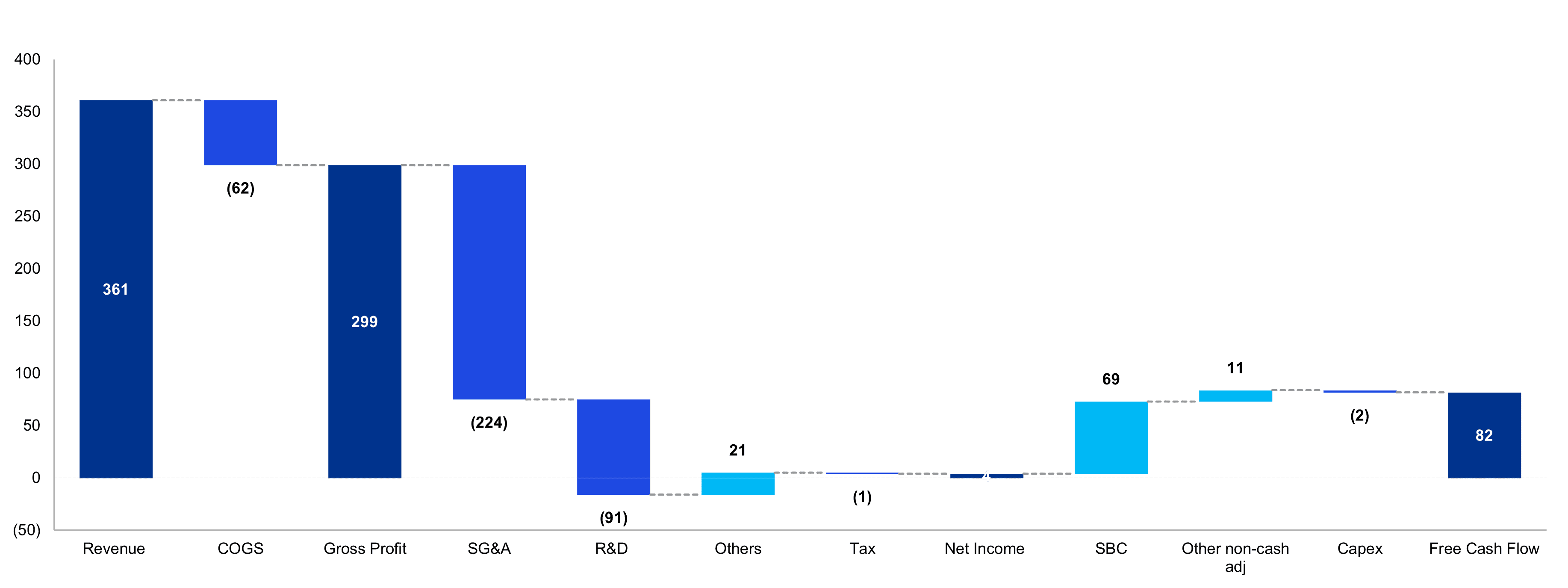

Revenue to FCF bridge (2023)

In the chart below i’ve shown the bridge from revenue to free cash flow in 2023. Highlights:

- Other Income: Primarily interest on cash balances driving positive variance between NOPAT/EBITDA and net income.

- Share-Based Compensation: Positive free cash flow in 2023 was largely driven by the add-back of SBC, indicating shareholder dilution.

It’s for this reason that i believe Free Cash Flow per share, or Free Cash Flow less SBC are the right metrics to focus on.

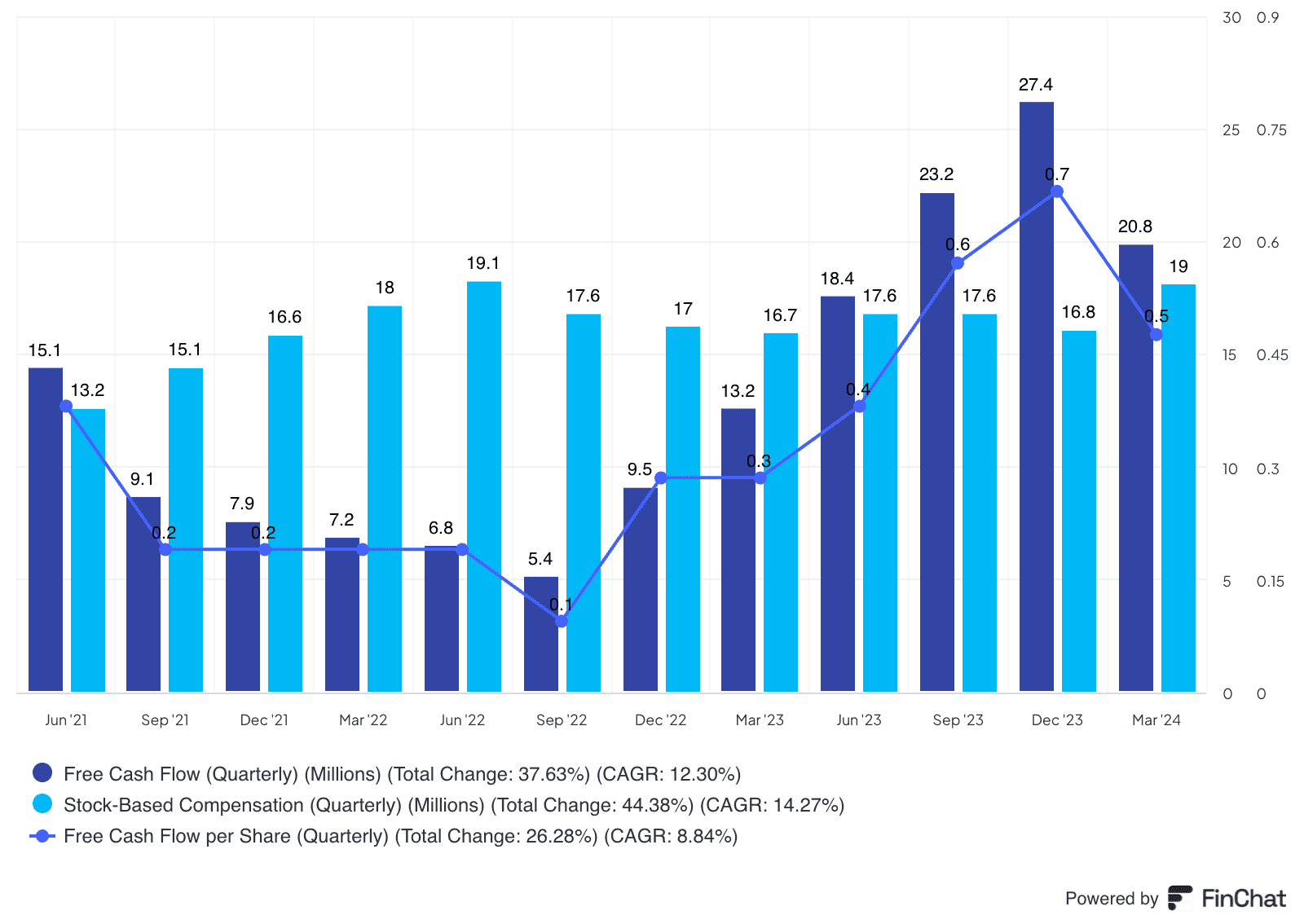

Free Cash Flow Per Share Development (quarterly)

The quarterly development of free cash flow per share (line chart) shows positive trends, although this reversed in Q1 2024 due to an increase in SBC.

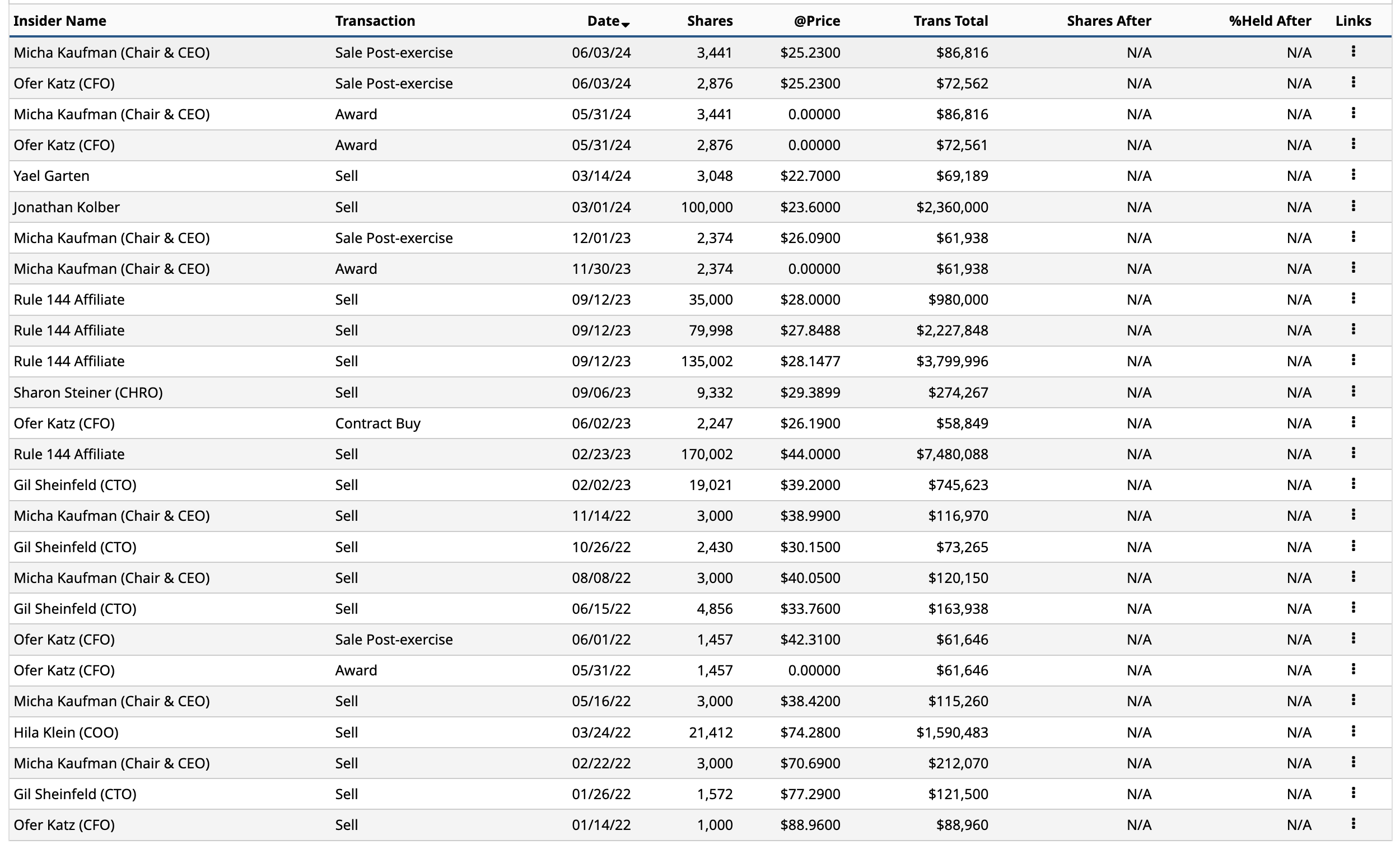

Management skin in the game?

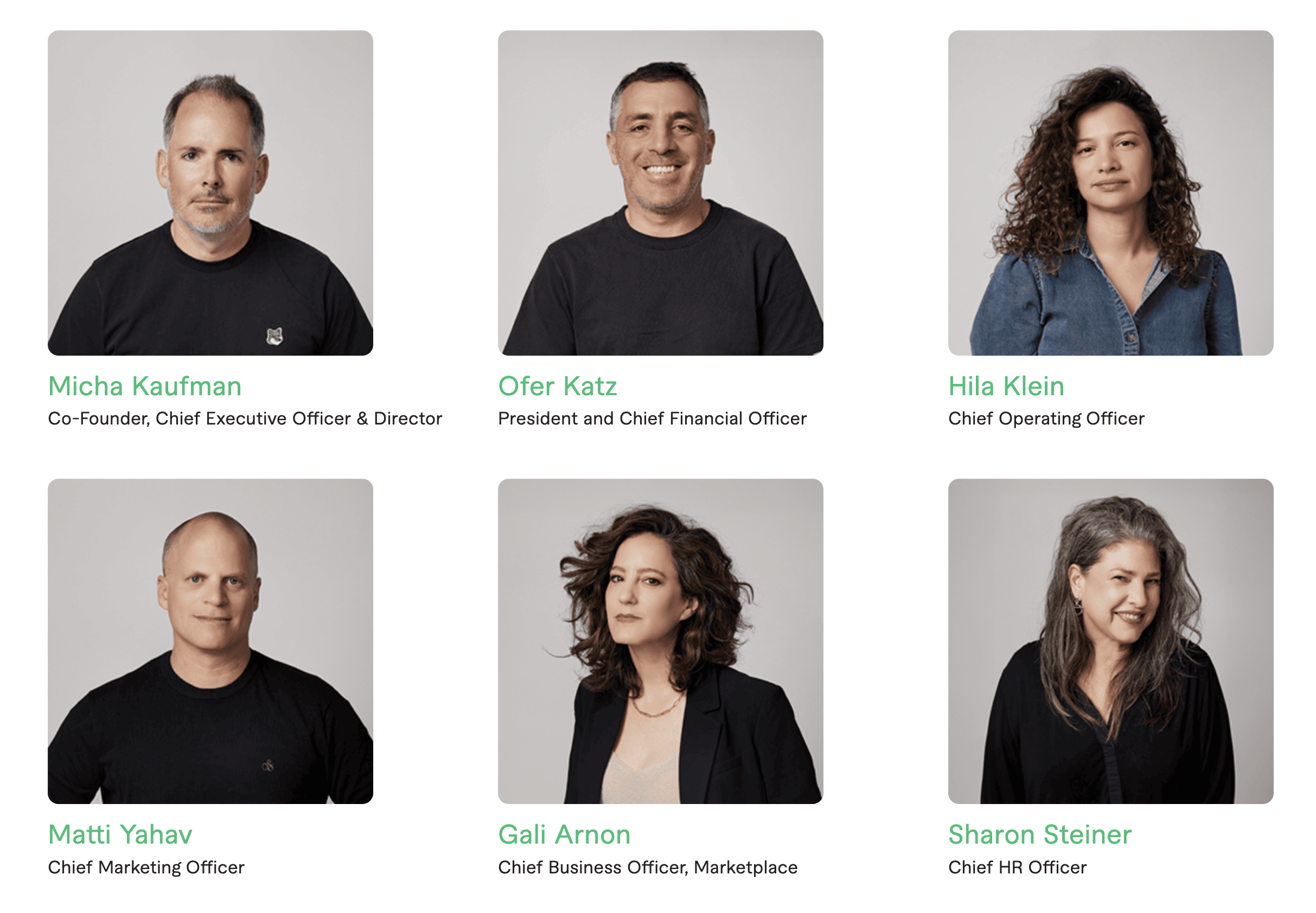

Fiverr is founder-managed, with significant insider ownership, indicating strong alignment with shareholders. The management team includes:

- Micha Kaufman, CEO: Holds around 6.6% of ordinary shares (worth approximately $66 million), with a weighted average exercise price of $60 for his 942k share options.

- Ofer Katz, CFO: Owns 1.1% (around $11 million), with a weighted average exercise price of $72 for his 204k share options.

- Jonathan Kolber, Board Member: An early investor, holding about 7.6%, down from a peak of 12.5% in 2020.

Insider Trading Insights

Recent insider trades show relatively small and normal sell-offs, primarily, I assume, to fund living expenses, which indicates no significant loss of confidence. The CFO’s purchase in February 2023 at $26 is a positive sign of internal confidence. Overall, the insider holding pattern suggests a strong belief in the company’s long-term potential.

Service categories and AI impact on the business

Fiverr categorizes services into simple, neutral, and complex, with complex services now accounting for over one-third of GMV. This shift towards more complex services is expected to continue growing rapidly.

Net positive AI impact?

Management views AI as a net positive, creating more jobs and opportunities. Key benefits they perceive include:

1. Growth in AI implementation services

AI continued to have a net positive impact on our business, as complex services continue to grow faster and represent a bigger portion of our business. Demand for AI-related services remained strong, as evidenced by 95% year-over-year growth in GMV from AI service categories. Chatbot development was especially popular this quarter as businesses look for ways to lean into GenAI technology to better engage with customers.

With an over 10,000 and growing AI expert pool, Fiverr has become the destination for businesses to get help implementing GenAI and take their business to the next level.

Micha Kaufman – May 2024 earnings call

2. Improvements in the matching buyers and suppliers using AI

We have also seen very promising signals on Fiverr Neo, the AI matching assistant that we launched last year. Neo enables our buyers to have a more natural purchasing path by creating a conversational experience that leverages the catalog data and search algo.

Micha Kaufman – May 2024 earnings call

Answers and steps are provided based on buyers’ questions and the stage of the search. As a result, we saw that nearly 1/3 of the buyers who received seller recommendations from Neo ended up sending a project brief to the seller and the overall order conversion is nearly 3x that of the marketplace average. MK

3. Rise in on-platform data

In 2023, over 38 million files were exchanged on our platform, and on average, 2.5 million messages were sent between buyers and suppliers. MK

Micha Kaufman – May 2024 earnings call

Potential Disruption by AI

However, clearly AI will be cannibalising legacy services (as is the case across many industries). Contrasting this optimism, this is a quick list of services currently offered that i think will be disrupted/cannibalised by AI:

- Logo Design

- Article writing

- Copywriting

- Social media graphics

- Translation services

Overall View on AI:

While AI may cannibalize some legacy services, it also opens new opportunities for freelancers to adapt and leverage AI for more complex and higher-value tasks. Offering AI implementation services positions Fiverr well in a market where traditional technology consultants focus on large enterprises, leaving SMEs to seek freelance solutions.

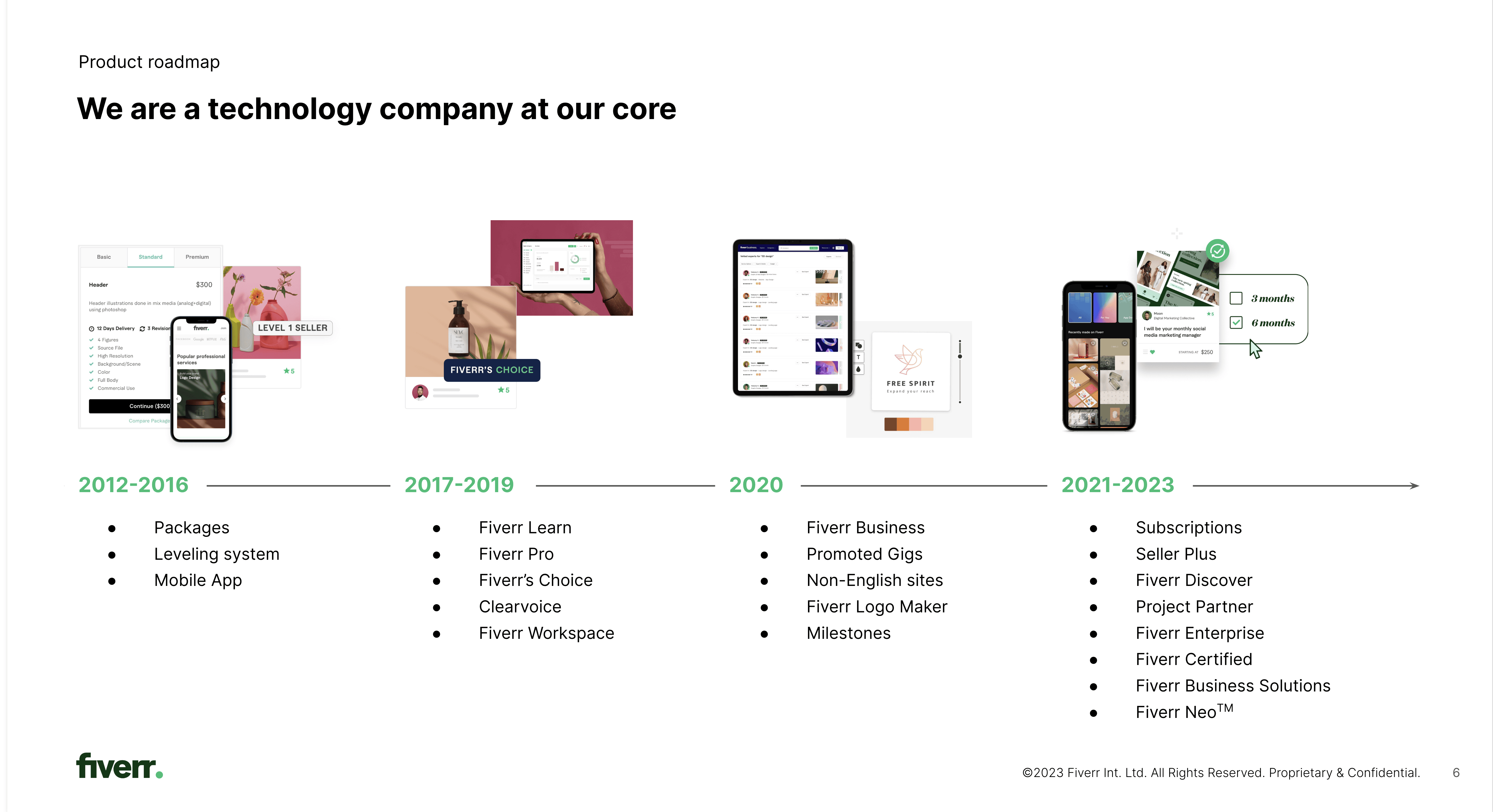

Product Innovation

This is the product development roadmap from the latest corporate presentation.

The latest products are:

- Fiverr Neo – i.e. more sophisticated matching of buyers and suppliers using AI

- Business Solutions offerings such as Fiverr Certified and Project Partner – i.e. Looking to drive a shift towards more complex products on Fiverr focussed on larger customers.

Fiverr is developing tailored customer experiences for mid and large businesses, including pairing clients with consultants and providing account management support to foster long-term relationships. I think this is a key area to watch.

Employee engagement

Despite the ups and downs in share price, Glassdoor ratings are pretty solid: 83% approval rate, and 91% approval for the CEO.

Fiverr community engagement

Community Engagement Strategy

Fiverr employs a vetting process combining technology and human reviews to ensure high-quality work from freelancers, particularly in complex services. The company actively engages with its community through a dedicated forum, where users can provide feedback and suggestions.

Key Community Insights

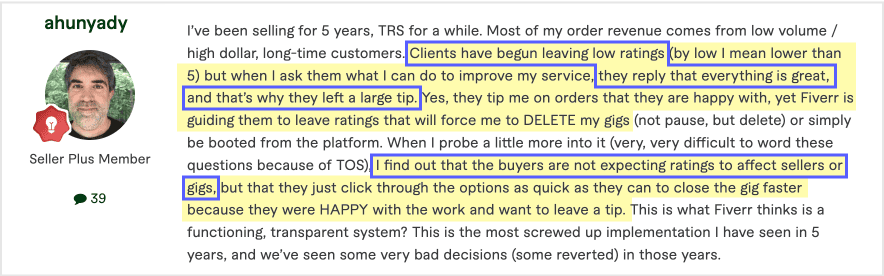

Useful information on the fiverr community can be found at their community page here. My observations from reading the community pages are the biggest topics are:

- Seller Rating Systems: The rating system for sellers is a critical aspect of Fiverr’s platform. It is a key internal KPI that impacts seller performance and buyer satisfaction. There is a view from a number of sellers that the rating system is misleading / unfair.

- UI and UX Improvements: There are ongoing requests for UI and UX enhancements, such as dark mode for the mobile app and more intuitive dashboards and metrics.

- Payment Options: Sellers have requested more payment options to reduce processing charges, which would enhance their overall experience on the platform.

- AI Tools: Fiverr is pushing sellers to leverage AI tools to increase efficiency and improve the quality of their services.

Markets & Competition

Fiverr faces several competitive threats in the freelance marketplace, categorized into direct competitors, niche and specialized platforms, emerging technologies, economic and market conditions, and customer preferences and trust.

Direct Competitors

- Upwork: A major competitor, Upwork targets more complex and long-term projects with an extensive vetting process and project management tools.

- Freelancer.com: Offers a wide variety of projects and has a global reach, posing a significant competitive threat.

Niche and Specialized Platforms

- Toptal: Connects businesses with top-tier freelance talent in software development, design, and finance, attracting premium clients.

- Guru: Focuses on long-term projects and offers workrooms for project collaboration.

Emerging Technologies and Trends

- AI and Automation: The rise of AI tools that can automate various tasks traditionally done by freelancers poses a threat, especially in content creation, graphic design, and customer service.

Economic and Market Conditions

- Economic Downturns: Recessions can reduce the demand for freelance services as businesses cut back on spending.

- Regulatory Changes: Changes in labor laws and regulations could impact Fiverr’s business model.

Customer Preferences and Trust

- Trust and Quality Concerns: Maintaining high-quality standards and trust within the platform is crucial. Lapses in quality control or incidents affecting trust can drive customers to competitors.

- Customization and Flexibility: Clients demand more customized and flexible freelance solutions, which can attract more clients if platforms offer better project management tools and seamless communication.

Comparing Fiverr and Upwork

Fiverr: Known for its user-friendly interface and affordability, ideal for quick, one-off tasks. Operates on a gig-based system where freelancers post predefined services.

Upwork: Better suited for larger, long-term projects requiring detailed planning and collaboration. Features a more extensive vetting process and project management tools.

Key metrics comparing both show the following:

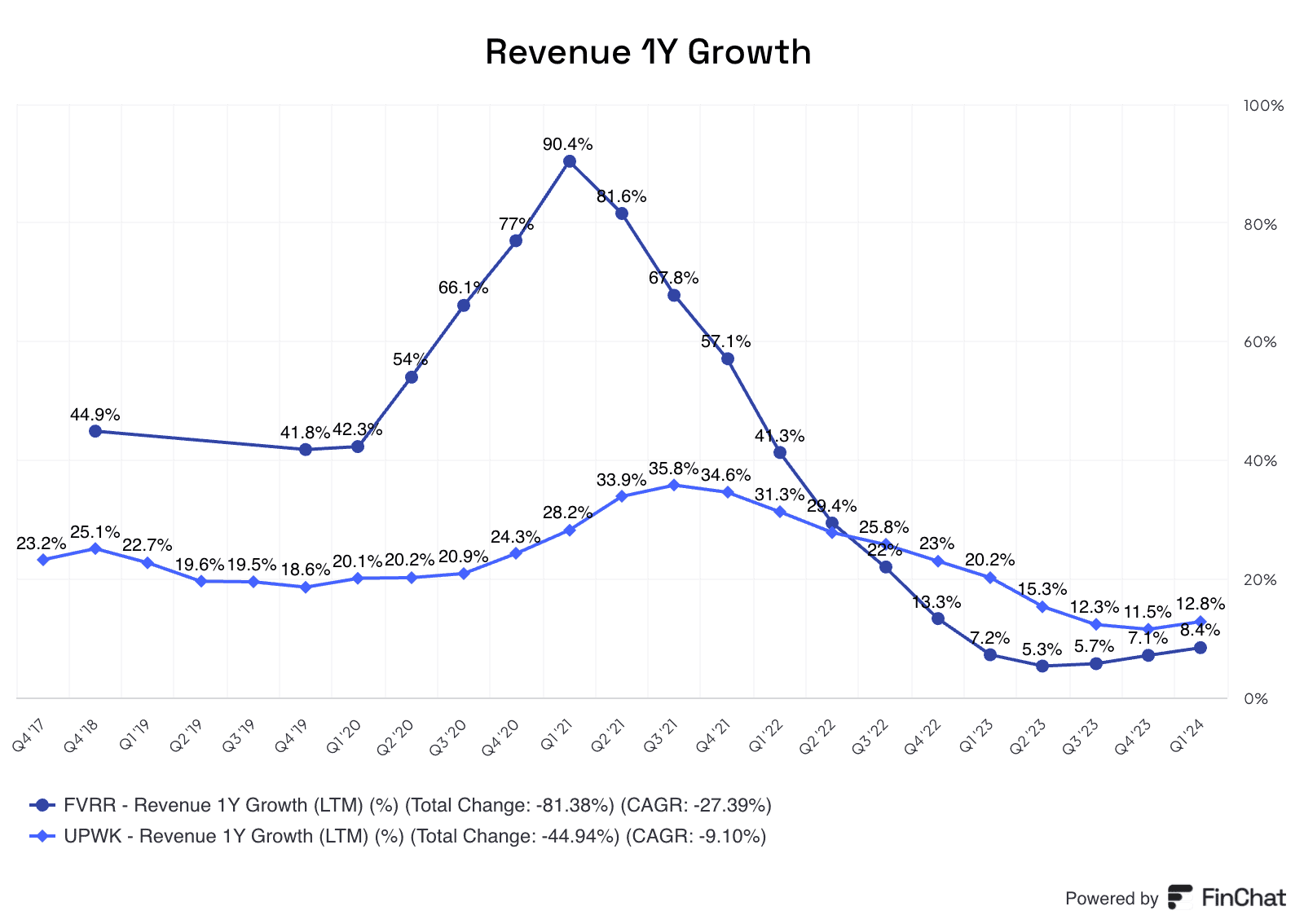

- Growth Trends: Fiverr experienced higher initial growth but faced faster deceleration. Upwork showed consistent revenue growth with slower deceleration.

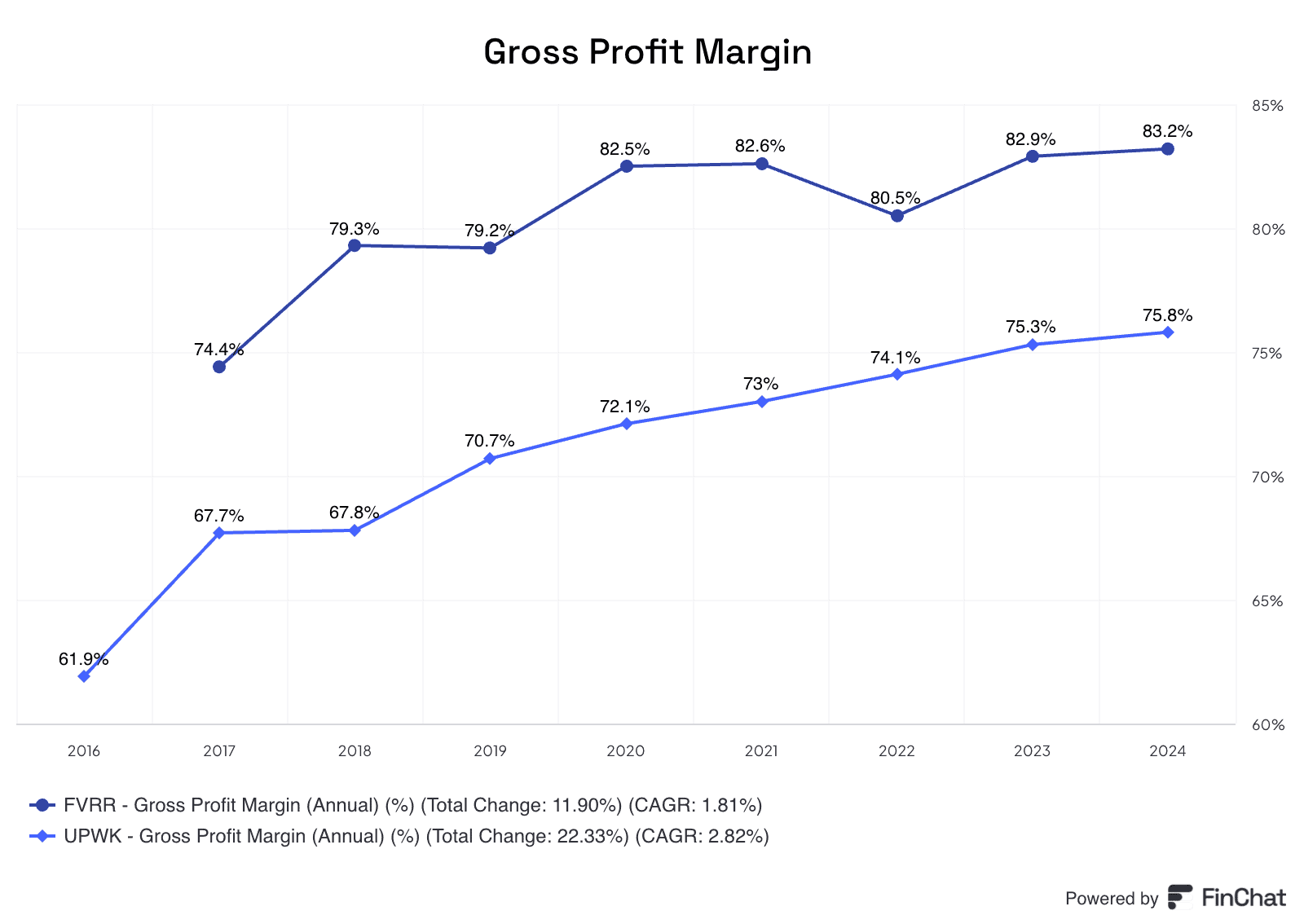

- Margins: Fiverr’s gross margin is about 8 percentage points higher than Upwork’s, reflecting Fiverr’s higher take rate (30% vs. 19%).

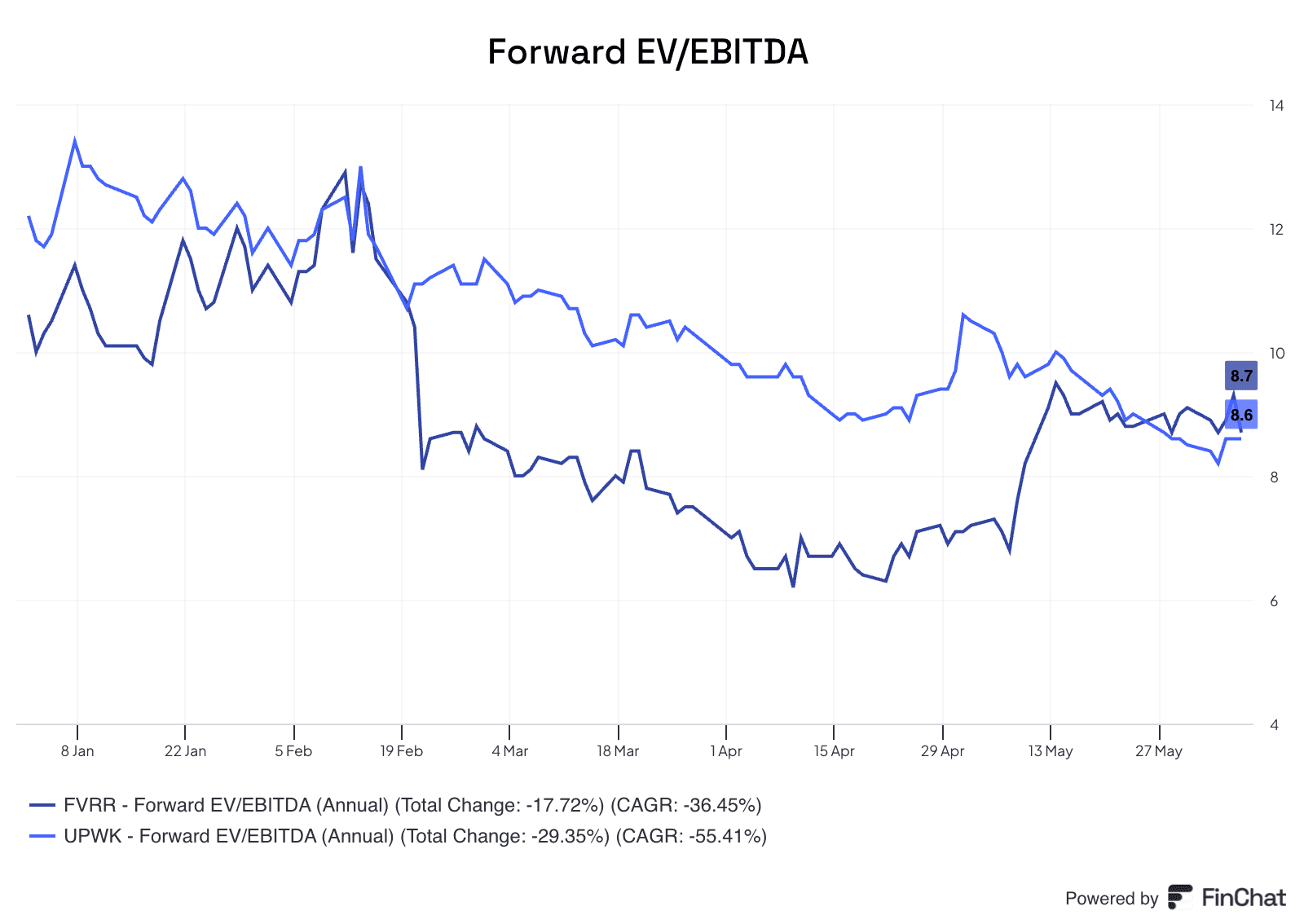

- Valuation: Both companies trade at similar forward EV/EBITDA and EV/FCF multiples, though Fiverr’s EV/FCF valuation is slightly lower due to higher share-based compensation overhang.

- Share Buyback Programs: Both Fiverr and Upwork have initiated share buyback programs, reflecting confidence in their respective stock valuations.

Growth trends

In May 2024, Upwork raised both revenue and adjusted EBITDA guidance for 2024. Fiverr did the same in May 2024. This implies they will be hitting 10%+ growth rates in the coming quarters.

Margins

In terms of margins, we see a see c. 8 percentage point higher gross margin in Fiverr than Upwork, reflecting Fiverr’s significantly higher take rate (c. 30% versus c. 19% for Upwork).

Valuation

Both companies trade at similar forward EV/EBITDA (c. 8.5x) and EV/FCF multiples (c. 6 – 8x), although Fiverr’s valuation is slightly lower due to higher share-based compensation overhang.

So our EBITDA converts to free cash flow at a very high rate, call it 90%. So we will be producing growing free cash flow. We also obviously think the stock is pretty undervalued at these levels. We just bought back $100 million of stock in the past few months. And so we are going to be continuing to look at options with our balance sheet.

Erica Gessert, Upwork CFO, May 2024

Conclusion

Fiverr and Upwork present compelling investment opportunities in the freelance marketplace. Fiverr’s strong fundamentals, growing free cash flow, and strategic initiatives position it well for future growth despite challenges like share-based compensation and potential AI disruption. Upwork’s consistent growth, extensive vetting process, and project management tools make it a strong competitor. Both companies are leveraging AI and product innovations to enhance their platforms and attract more clients.

I believe both FVRR and Upwork are buys for a long-term investor at current prices. I plan to increase my position in Fiverr and start a new position in Upwork, viewing these as long-term investments (i.e., several years rather than months).

Investment Thesis for Fiverr AND Upwork

- Attractive Valuations: Both stocks are undervalued due to concerns about AI disruption, providing an opportunity for long-term growth.

- Growing EPS and FCF per Share: Both companies are showing growth in earnings per share and free cash flow per share.

- Revenue Re-acceleration: Indications of re-accelerating revenue growth enhance the attractiveness of these investments.

- Robust Balance Sheets and Share Buybacks: Both companies have strong balance sheets and are executing share buyback programs, signaling confidence in their valuations.

Risks for Fiverr AND Upwork

- AI Disruption: While AI presents growth opportunities, it also poses risks by potentially cannibalizing certain freelance services.

- Macroeconomic Conditions: The global economic landscape is volatile. However, I believe it is bottoming out, and I do not foresee significant further declines.

Which is better positioned re AI: Fiverr or Upwork?

Fiverr: Reported a 100% growth in AI services GMV, focusing on areas like chatbot development, model training, and prompt engineering. This suggests an ability to adapt and leverage AI for growth, and demand from clients.

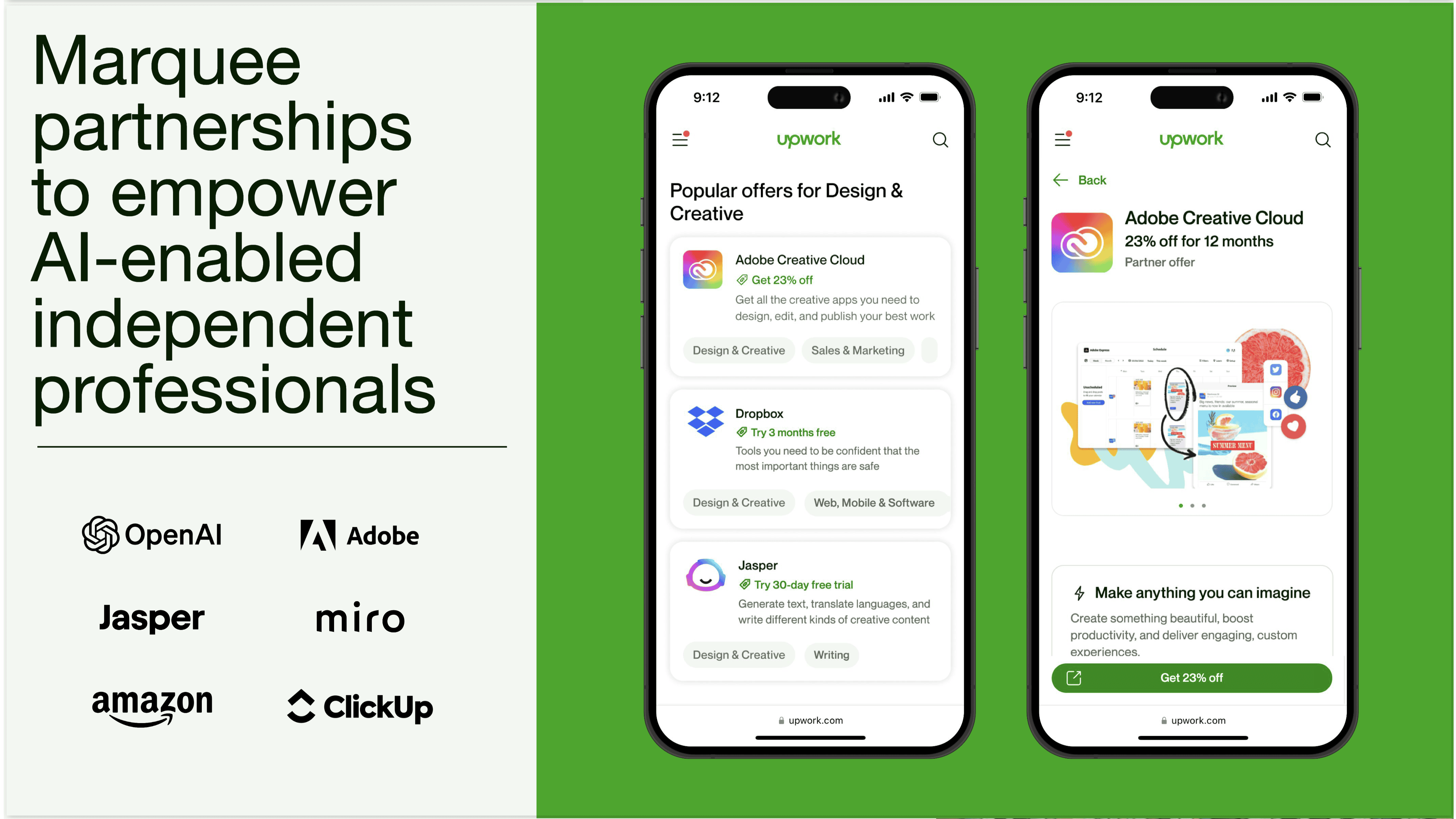

Upwork: Touted 50% growth in its AI & Machine Learning category. Upwork also acquired Headroom in 4Q23, enhancing its AI strategy. Upwork appears well-positioned to offer AI implementation services, with data showing higher utilization of AI tools among freelancers compared to internal employees.

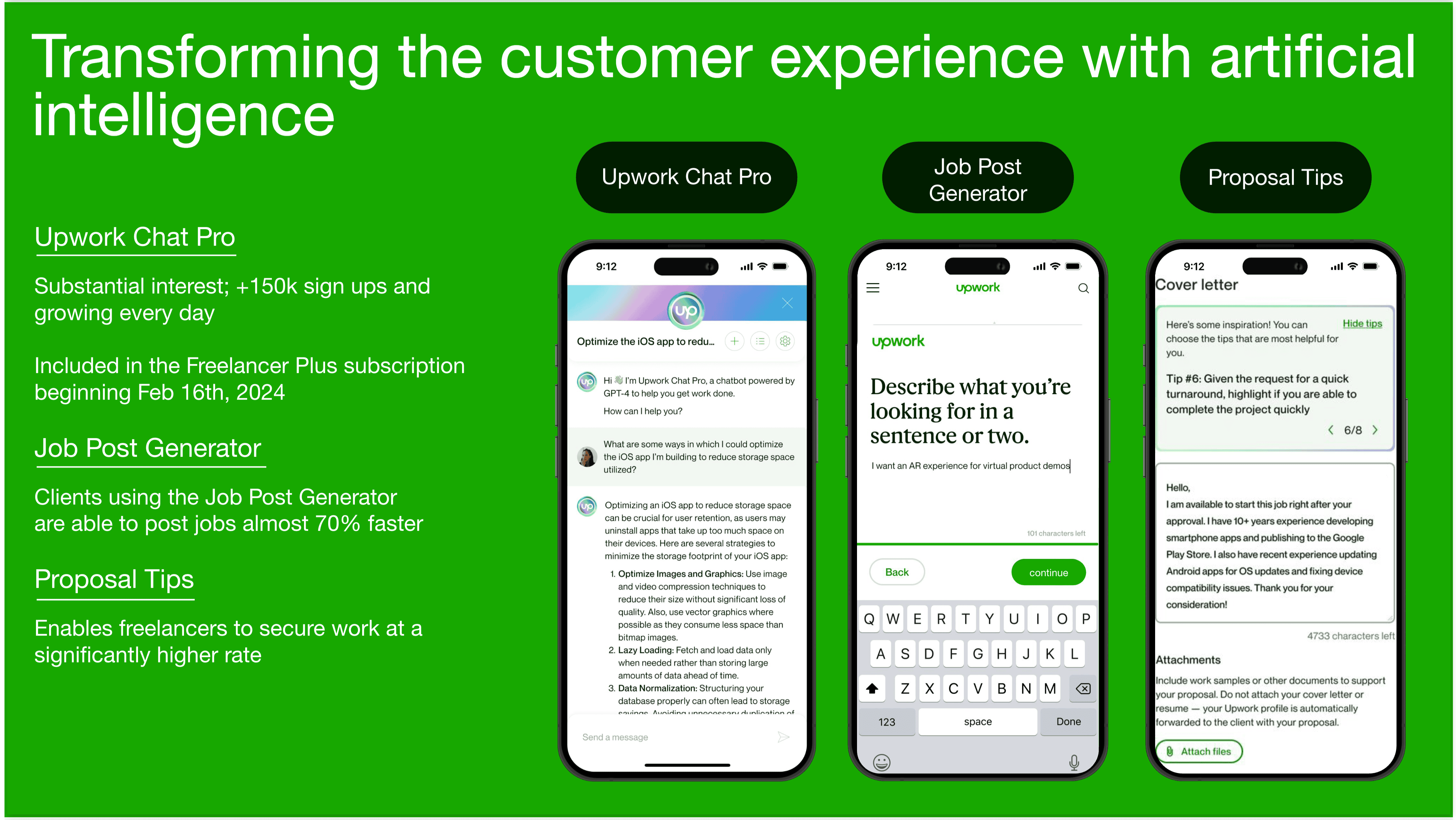

Extracts from recent Upwork investor presentations on AI

And I think the interesting fact there is the data shows that only about 9% of internal employees are using AI tools on a regular basis compared to 20% of freelancers and compared to more than 50% of freelancers on Upwork who are equipped and using these tools.

Erica Gessert, CEO of Upwork

While I think Upwork may have an edge in selling AI implementation services, Fiverr’s reported growth in AI services cannot be overlooked. Ultimately, both platforms can potentially turn the perceived AI headwinds into tailwinds, making them strong candidates for long-term investment.